Writing's on the wall

New write-up: Soilbuild Construction (V5Q.SI)

Overview

Soilbuild Construction is a growing Singaporean company, offering end-to-end construction of complex buildings in the residential and the industrial sector. It has constructed buildings like the Soitec semi-conductor production factory, DB Schenker’s award-winning green Logistics Hub, and the Verticus 162-flat skyscraper in Singapore.

The company has just reported 273m in H1 2025 revenue (+77%), and 28m in H1 2025 earnings (+280%). We think this growth is likely to continue in the coming years, as Soilbuild had H1 2025 new bookings of 360m, growing their order book to ~1.2B, covering about 2 years of forward revenue growth, with more new bookings (award wins) continuing to come in.

The stock is priced at 5.8x TTM net earnings, or 4.8x H1 earnings annualized, or ~3.8x after backing out the cash. (Owners’ earnings look even slightly better, as the company is depreciating some of its factories, but is using very little capex.)

In this pitch, we cover the background of the company, their recent inflection driven by a new CEO coming on board in 2023 and modernizing the business, the valuation, ownership structure, and the risks.

What does the company do?

Soilbuild Construction Group was started in 1976, currently has ~988 employees and is engaged in 2 main activities:

Industrial, residential and public real estate construction (81% of FY24 revenue)

Expertise includes building residential, commercial, and industrial structures, public housing, schools, and institutional facilities. This business unit takes care of the end to end building process, including design, procurement, project management, construction management, and installation of utilities. Example clients are DB Schenker, Pall, Leica and the Singaporean government.Pre-cast concrete manufacturing (19% of FY24 revenue)

Soilbuild Precast & Prefab, manufactures precast concrete and steel components in Singapore and Malaysia. The components are sold to Soilbuild’s construction business unit, as well as to external customers. Example clients are the Singaporean housing board (HDB) and Soilbuild’s construction BU.

Quick context on Singapore (skip if you know what kaya toast is)

Singapore is a country of 6 million inhabitants, with a diversified economy that thrives thanks to an excellent education system, pro-business government and great infrastructure.

The country has a 35% trade surplus, 4% real GDP growth, just under 2% inflation, a balanced fiscal budget, and friendly relationships with China, India, Europe, the US and Japan. One SGD is about 0.75 USD. This currency pair has kept a relatively narrow range since 2010. (+/- 10%)

The economic success of Singapore leads to increasing public and private infrastructure investments. Singaporean construction demand is estimated at ~43 billion SGD in 2025.

The Soilbuild empire built by Mr. Lim

Mr. Lim Chap Huat founded Soilbuild in 1976 with 2 co-founders. The 22-year-old engineer, third of seven children of a trishaw rider and washerwoman, grew up in poverty. He funded his studies by working part-time as a teacher, and founded the company using 5k SGD in personal savings, but grew it into 3 large branches over the past 49 years:

Soilbuild REIT, A Real Estate Investment Trust, of which most assets were bought out in 2024 making Mr. Lim a billionaire.

Soilbuild Corp., focused on property development and management, owned by Mr. Lim

Soilbuild Construction (V5Q.SI), focused on construction and engineering. Originally a subsidiary of Soilbuild corp., until being listed on the SGX in 2013 through an IPO. Mr. Lim still owns a large majority stake in the company and his son Lim Ran Hen became the CEO of the company in January 2023 after a history of different short term CEO’s with limited success.

While the three companies used to work together significantly in the past, their ties have weakened over the past years as we will see late on. The companies are currently not part of one capital group, although the ownership of Soilbuild Corp and Soilbuild Construction Group are similar, with Lim owning a large majority in both companies. Going forward, when we mention “Soilbuild”, we are referring to Soilbuild Construction (public co) rather than Soilbuild Group (private co).

Financial performance of Soilbuild Construction

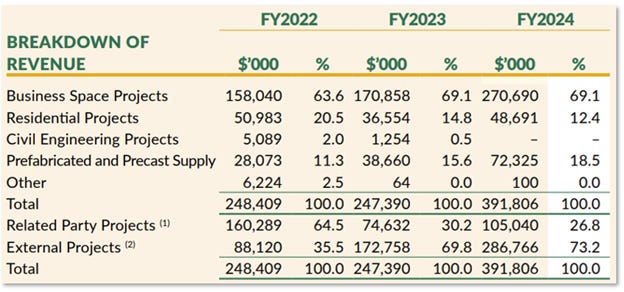

Soilbuild has a decent 3 to 10-year track record, inflecting into excellent performance over the past 6-24 months. Below is a breakdown of their financials from their 2024 Annual Report.

Notice:

Soilbuild is increasingly focusing on Business Space Projects, doing less residential (Commercial real estate is doing just fine in Singapore 😊)

BU Prefab & Precast Supply is growing & becoming a meaningful part of the business

Related Party Projects are becoming a smaller part of the business. These are Projects where Soilbuild Corp/REIT (the historical parent) is the customer. So, they are building for their own property management business in this case. This further declined to 12% in H1 2025.

External Projects are growing quickly. These are projects for external customers, based on actual sales effort, and where margins are probably more important. (from a majority shareholder perspective)

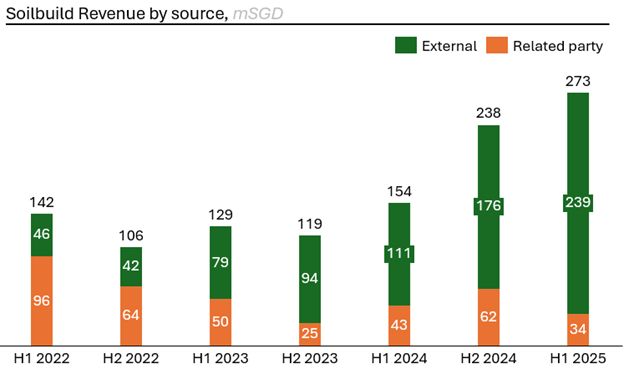

Below is a chart of External Project revenue vs. Related Party revenue showing the evolution of both types of revenue sources:

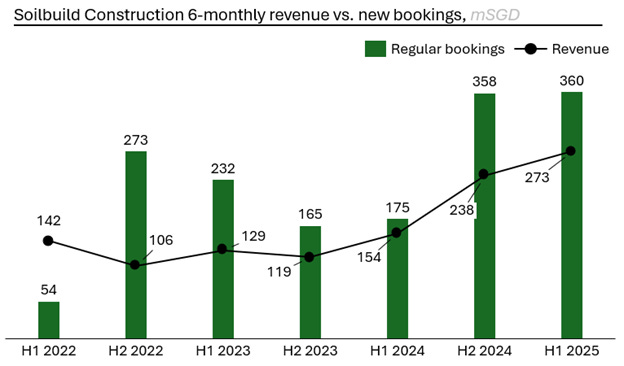

Revenue growth for a construction company can only last when driven by growing project wins (aka bookings) which provide an excellent leading indicator for growth. Soilbuild has consistently grown the value of newly won contract awards, and this has exceeded revenue for each of the past 6 half years.

These consistent wins have lead to an order book of 1.2 billion in projects to be executed - so the writing is on the wall in terms of upcoming revenue growth.

The bookings/awards in the chart above exclude a single huge one-off award of 647 mSGD in H1 2024, for the construction of a Supply Chain Hub at the Tuas port, for the Port Authority of Singapore (PSA). We have excluded this massive win, to show that even without it, Soilbuild is a nicely growing business.

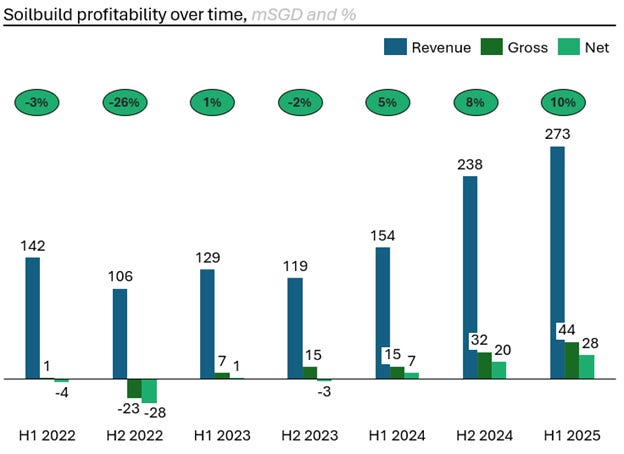

Looking at the bottom line, as Soilbuild moves to greater revenue share from External Projects, it increases its profitability, leading to ~48 mSGD net earnings for the past 12 months.

Hearing about this success story, it’s normal for one to look up from their Mahjong game, put aside their Laksa, and ask…

What is driving their success?

The clear inflection in performance was delivered under the leadership of Lim Han Ren, 33-year-old son of the founder, who has taken over the CEO role at Soilbuild in January 2023, working alongside his dad who remains the Chairman.

While it is difficult to identify his personal impact, Mr. Lim Han Ran has consistently stressed the importance of Digital Technology and Sustainability.

Soilbuild has implemented their improved value proposition through:

Setting up Building Information Modelling, and digital construction simulation (Digital twin)

Implementing CCTV analytics to improve construction site safety (AI camera’s)

Improving project delivery visualization for customer

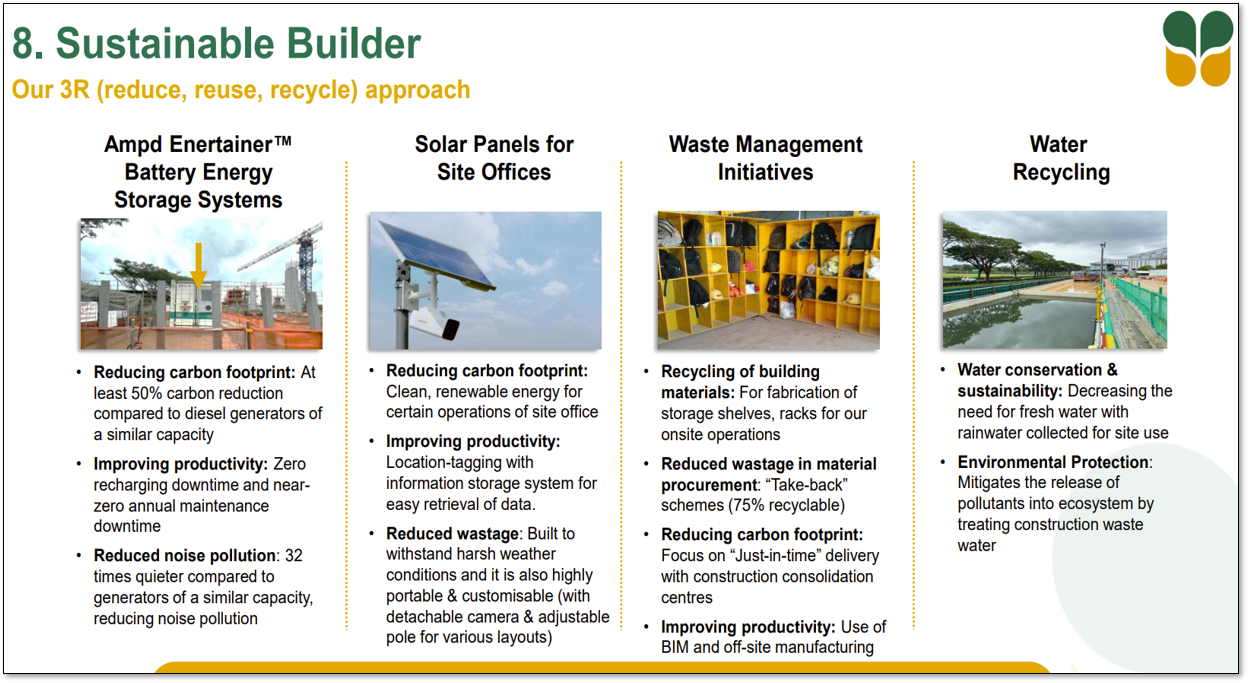

Integrating green construction initiatives (Solar panels, water recycling, battery cells instead of diesel power generation on site, waste reduction and recycling… )

Delivering green building designs (Improved insulation, improved design for energy efficiency, rain water use, sunlight columns …)

More of these types of slides showing Soilbuild’s specific Green and Digital value proposition can be found in its semi-annual report presentations, which have become a lot shinier and more interesting over the past 2 years.

This enables Soilbuild to win more prestigious awards with external customers, for example:

DB Schenker’s award winning advanced CO2 neutral Logistics Hub:

PSA’s Supply Chain Hub at the Port of Tuas:

We believe the improved value proposition is the main driver for the increase in external sales and margins, as customers choose a differentiated partner to run the design and delivery process of their prestigious buildings.

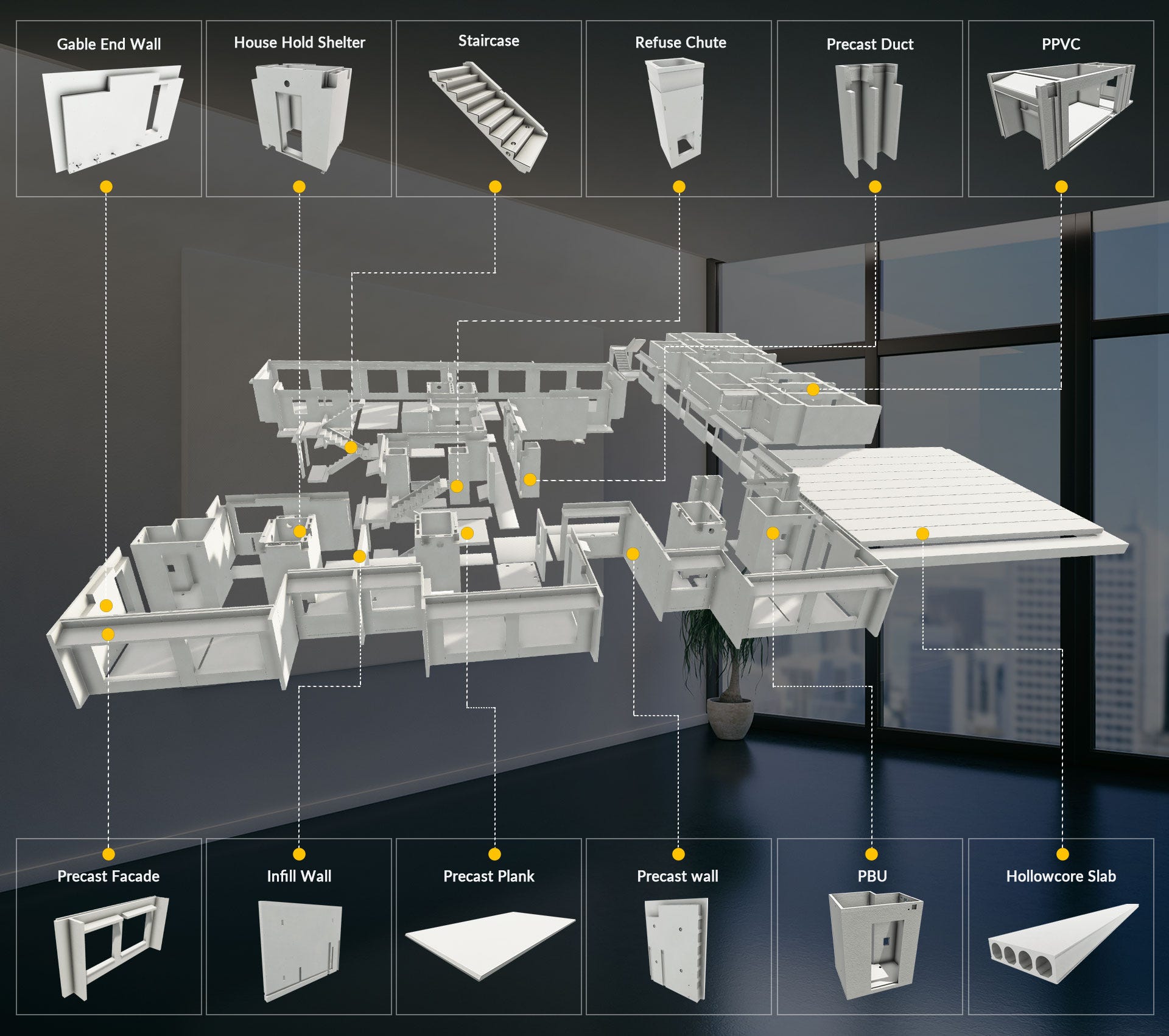

Besides the improved value proposition of the construction business unit, Soilbuild also has improved the capabilities of its pre-cast and prefab business unit. This BU can now produce a much wider variety of building parts, and provides standard libraries integrating with customers design tools, as can be seen below.

Valuation

We like to value a company based on its current earnings power, annualizing the past 6 months. To annualize earnings, we should have reasons to believe they will be higher (or equal) in the future. For Soilbuild, we think the strong order book and the improving margins driven by higher quality projects indicate profits are likely to grow with revenues in the coming years.

We think an ex-cash PE multiple of 10-15 is appropriate, reflecting a company with continued double-digit growth at healthy margins, delivering recognizable high-tech projects.

This leads to a market cap of 10-15 x 56m net income + 58m cash = 620-900 mSGD, corresponding to a share price of 4-5.8 SGD per share, a considerable surplus versus today’s 1.66 SGD.

We sometimes get asked if 10-15 PE is the right multiple for a growing company. It may or may not be, because it all depends on opportunity cost, but

Yes, we think 10-15x is fair for a growing business in a modern growing economy

If a growth company trades at 5-6x P/E forever, their share price rises as new contracts’ growth turns into profit growth. If they stay this cheap, they get ~15-20% earnings yield to fund buybacks/dividends and growth, which is not a bad position to be in. The multiple does not have to re-rate for the returns to be great

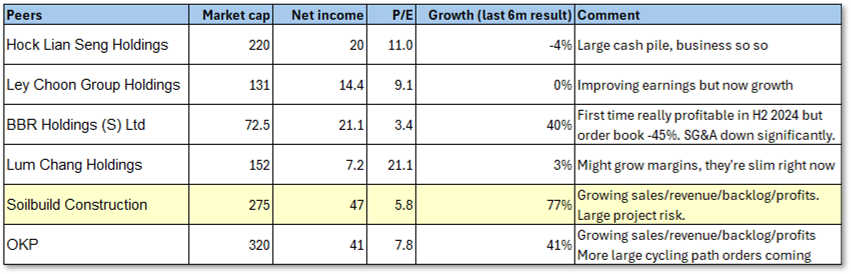

Comparative (small cap) analysis for a company like Soilbuild looks like the table below. We find some companies that are much more expensive for no obvious reason, and we find companies that look much cheaper/better. Reading the annual report for those in the second group however reveals some issues going beyond valuation. Each of the companies have their own specific capabilities and niches, making a comparison difficult.

As readers know, we are also invested in OKP. This company has 136m of cash on their balance sheet, which is about 80m more than Soilbuild, making the ex-cash multiple of both companies very similar. We think both companies are attractive in their own way, but we’re biased on both.

Ownership structure & Share structure

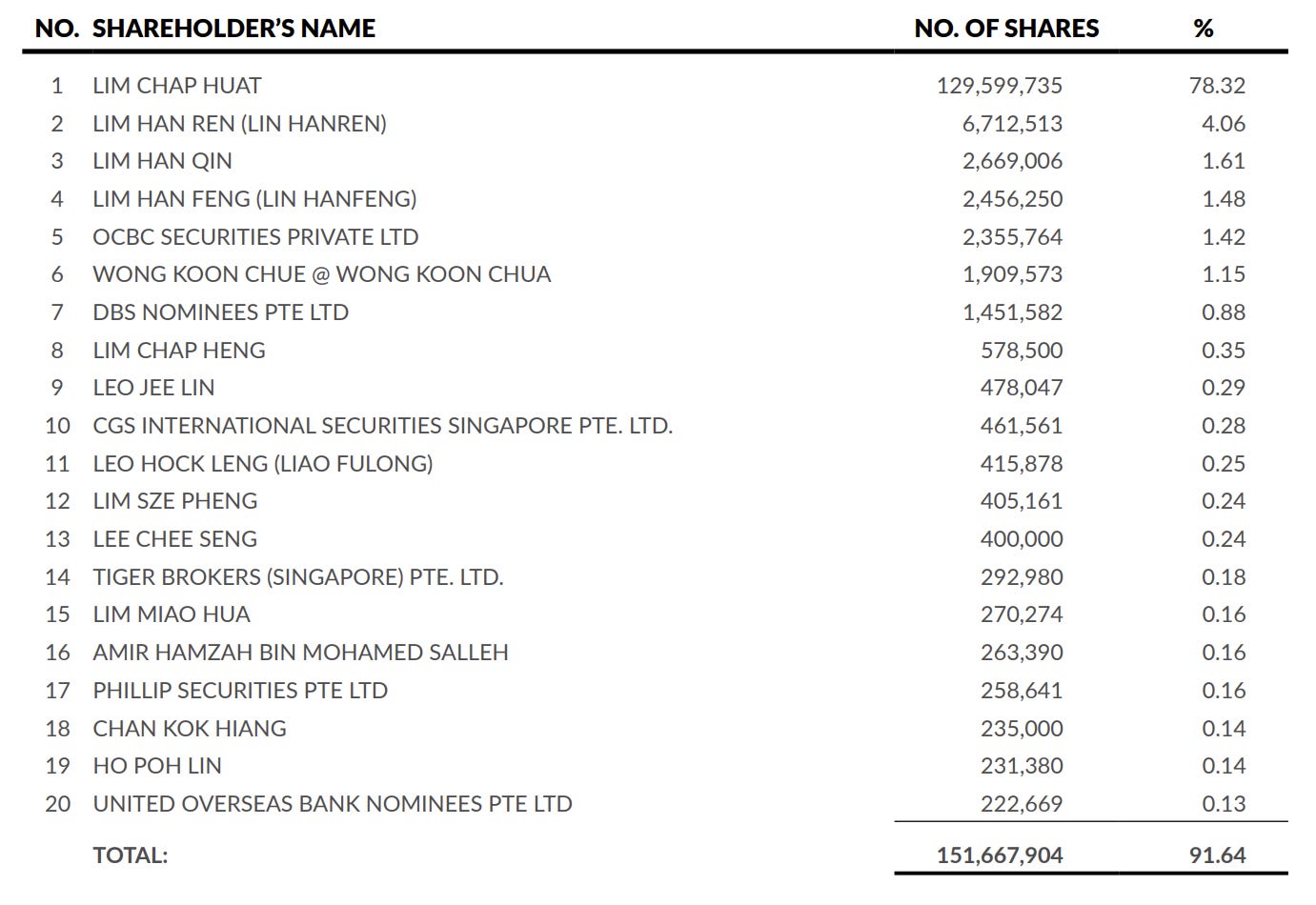

Soilbuild is majority owned by chairman Lim Chap Huat. The Lim family together owns ~85% of the company. Soilbuild today has no options/warrants. Historical warrants expired in July 2024. Soilbuild did conduct a 10:1 share consolation in December 2024.

The relatively high insider ownership is a watch out. If the Lims’ family ownership rises to 90% or higher, they could trigger a delisting offer at a “fair” price. This could prevent minority shareholders from capturing the upside in the company. So far nothing suggests this will happen but it’s important to watch this going forward.

We will not go into capital allocation here as the company has been splitting its profits between paying dividends and driving organic growth at ~30% ROE.

Risks

We think investing is risky, and while these known risks seem limited, it’s clear that one could easily lose a lot of money investing in a small foreign construction company. Be aware of the risks and size appropriately using your own conviction rather than mine. Some of the risks are:

Recovery of the Chinese construction market could cause prices for labor and material might increase significantly which would have at least a short-term negative impact on margins

Competitors could catch up to offer similar Digital & Green buildings as Soilbuild is doing, increasing competition and hurting margins for Soilbuild.

The large PSA project at Tuas could fail. As the project is significantly larger than what Soilbuild has done in the past, operational issues or stakeholder management issues could arise that prevent efficient completion of the project. Even if Soilbuild does everything well, significant delays caused by the customer or by other suppliers could cause inefficiency.

The stock ran up > 50% rather quickly recently on the back of contract wins. While earnings are up 280%, a stock moving so fast might have a serious pullback at some point. At least expect volatility and don’t get in if you can’t handle it.

Delisting/squeeze out could limit potential upside as insider ownership is high.

Disclosure

We have shares in Soilbuild Construction. We didn’t write this post to do your due diligence, but rather to document our own, and to share it with others that may point out gaps to improve our process. We do not talk to management, and we do not accept payment from the companies we cover.

Summary

Soilbuild is a leading Singaporean construction company with growing order book, revenue and margins, driven by an improved value proposition centered around improved Digital and Green capabilities.

Despite its growth and clean balance sheet, Soilbuild trades at just ~5.8x earnings or 1.66 SGD per share. This is a deep discount to fair value of SGD 4 - 5.8 SGD per share.

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Do your own research.