DBA Group $DBA.MI

Original write-up 19/07/2024 (3.00 EUR)

Ticker: DBA.MI Price EUR 3.00

Shares Outstanding: 11,041,400 (excl. 471.900 treasury shares)

Market Cap: EUR 33m Net Debt: EUR 9m

Summary

I think DBA is an interesting investment, for 4 key reasons:

The business is founder-led and has a consistent track record of decades of revenue growth

Management has laid out an ambitious 2026 business plan, increasing growth in digitization and energy transition, while continuing growth in existing verticals, and increasing margins (budgeting 22% EBITDA growth per year)

The company is delivering ahead of plan in 2023 with 2023 EBITDA growth of 133%, and continued momentum in 2024, despite a weak construction and consulting climate in Europe

The stock is cheap at ~6x TTM earnings ex cash: (33-9)/3.8 = 6.4x

DBA group is a highly consistent, growing, successful engineering consulting company, which is well-positioned to deliver on Europe’s priorities in digitization and energy transition, driving higher recent growth and margins for the company. Shares trade at a forgotten 6x multiple, driving the founders to buy back stock.

1. Decades long founder-led track record

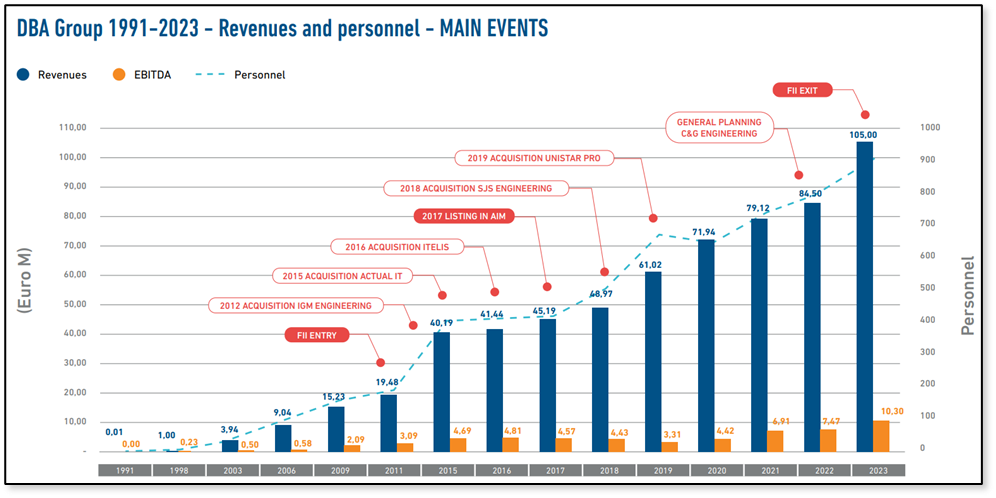

DBA was founded in 1991 as “De Bettin Associazione”, named after the 4 founding brothers, Francesco, Raffaele, Stefano and Daniele, 2 engineers and 2 architects. After initially focusing on architecture and design, the brothers quickly founded “DBA projects” in 1993 to focus specifically on project management and delivery of their designs for clients.

While initial growth was very slow, and projects were mostly driven by the 4 brothers in the beginning, the company expanded consistently since 1998, with mostly organic growth boosted by acquisitions.

Through the years, the company has grown its architecture and project development pillars, while adding IT and digitization as additional strategic sources of revenue. While part of this diversification was organic, it was aided by the small acquisitions of Actual IT, a Slovenian IT company, and Unistar, a cybersecurity specialty firm.

The brothers still own a controlling stake in the business, and each work at key positions at DBA (CEO, Chairman, Board member, Director of subsidiary). The company currently has offices in Italy, Albania, Bosnia and Herzegovina, Croatia, Montenegro, Serbia, Slovenia. They recently also did a bit of work in Azerbaijan, linked with the Italian embassy, and have also started supporting a customer in Canada this year.

2. The 2026 business plan

DBA builds on a long track record of digitization, which is becoming increasingly important. In mid-2023, after picking up more and more projects linked to the digital priorities (and problems) in Europe, Raffaele laid out DBA’s strategy, with

Objectives:

- Grow from 85m revenue in 2022, to 135m in 2026, mainly through organic growth, complemented with opportunistic acquisitions

- Expand EBITDA % margin from 8.5% in 2022 to 11.7% in 2026, through efficiency improvements, and fixed cost operating leverage (basically keeping fixed cost near stable while growing the business 60% in 4 years)

Verticals to reach +50m growth by 2026:

- Energy transition (+11m), with growth in both energy efficiency consulting for companies and communities, as well as the design and project management of new hydrogen distribution plants

- Digital transition (+7m), with growth in Datacenters. Over its history, DBA has led the design and delivery of over 50 data centers in Europe. DBA has announced multiple new large data center projects, making this a key area of growth going forward.

- Energy transmission (+6m), driving investments in charging infrastructure (mainly for harbors/ports to enable electric ships) as well as expansion of the electricity grid to enable data centers, ev charging and renewable energy sources to work together properly

- Other organic growth (+7m), in construction and ICT projects

- 2023 acquisition of General planning (+10m)

- Other M&A (+9m)

To enable this growth from a cash point of view, the company aims to improve margins and improve working capital efficiency, by streamlining its operating processes. This will enable self-funding growth and improved profitability.

It’s interesting to note that cybersecurity was not mentioned as a separate priority for growth, although this represents 25% of the company’s revenue.

3. Delivering 2023 well ahead of plan

While sharing their ambitious 2026 plan, DBA was already busy overdelivering it. For 2023, the company reported:

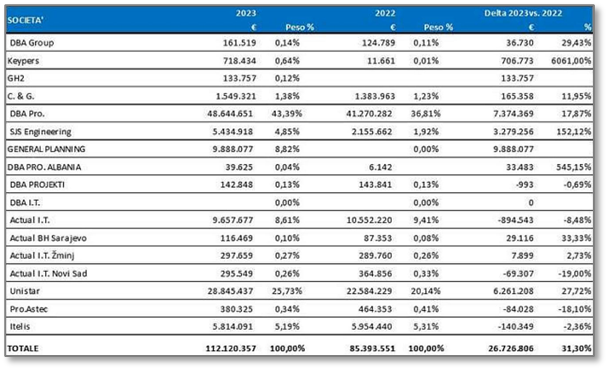

- 32% revenue growth, from 85 to 112 mEUR, of which 20% organic growth

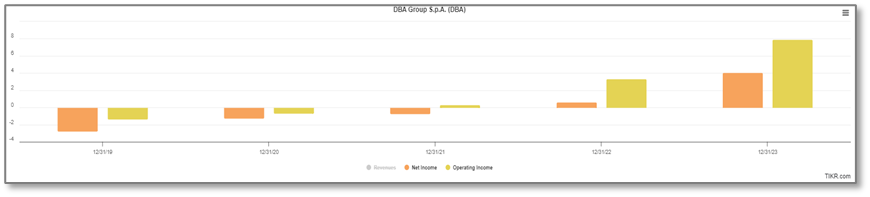

- 133% EBIT growth, from 3.4 to 7.9 mEUR

Looking at the composition of the group, we see a bit of a good co bad co situation, with:

- In-organic growth with General planning (and Keypers)

- Strong organic growth in DBA Pro (+18%) which is the core project development and project management business, and Unistar, the cybersecurity sub (+20%)

- Leap-forward growth (+152%) in SJS Engineering, which is the subsidiary providing port electrification (enabling ships to plug into ports to reduce emissions while docked, sometimes called cold ironing)

- Declines in Actual IT (8%), a Slovenian IT subsidiary acquired in 2015, reflecting the general drag in the market for IT consulting. Actual IT also has a ~3mEUR project digitizing the Serbian courts which closes in 2024. The company does not state whether any revenue of this project was recognized in the 2023 results.

The growth continues in 2024, with the company originally guiding for 4% additional revenue growth and 13% EBITDA growth in December 2023 and updating this in May 2024 to at least 8% revenue growth and 24% EBITDA growth, extending a long track record of growth, and beating and raising of expectations.

4. Low valuation

In terms of valuation, I like to look at (mkt cap – cash)/(Net Income-Financial Income) as a cash-adjusted TTM PE ratio. For DBA this is (33-8.8)/(4-0.2) = 6.4x

This is incredibly cheap for a company with this growth record and being well positioned to play into new industry trends in cyber security, data center expansion, electrification, and energy transition.

It’s great to see that management is taking advantage of the situation. They have bought back 4% of the shares outstanding in 2023 and have recently approved additional buybacks.

Looking a bit further into the financials, I observed:

- Margins are very thin but improved materially each of the past 5y and are set to increase further in line with the 2026 plan (same with ROIC)

- Earnings are understated, as the company amortizes goodwill at a fixed rate of 10% of gross asset value (straight line method / not based on impairment test).

(I think this might be a reason why the effective tax rate is higher than expected, but I’m not completely sure.)

While amortization of intangible assets sometimes reflects reality (e.g. for software, patents), it is not often the case for amortization of goodwill. As we have seen, the businesses DBA has acquired have generally continued to grow in revenue and in value. Therefore there is no reason to adjust their goodwill, and even less to reflect such adjustments in the income statement.

Buffett writes about this in 1983: "In analysis of operating results – that is, in evaluating the underlying economics of a business unit – amortization charges should be ignored."

Ignoring amortization of goodwill (1.5m in 2023 and 1.4m in 2022) shows the true earnings power of the business. Adjusted net income (owner’s earnings, right, fellow owners?) is then (4-0.2+1.5) = 5.3m for 2023

TTM Owners Price/Earnings is then 4.6x, and forward owners PE is ~4x only.

Risks

Every investment is risky, particularly a micro-cap equity investment like this one. We can think of a couple of specific risks to DBA:

1. One-off performance. It’s possible that the past 12 months of strong growth and margin expansion are one-offs, driven by luck in larger projects. I think this risk is quite large, but the potential impact is mitigated by the low valuation of the stock. They will deliver record revenue and earnings again this year and will likely continue to do so several years into the future.

2. Margin compression. With net margins of only 4%, the company’s earnings might disappear quickly. That said, I do think this risk is limited, just looking at the track record of the last 5 years, in which we have seen everything from deflation, inflation, growth, recession, covid, … in Italy. The company has consistently increased and beaten its targets through this period leading to rising EBIT and net income.

3. Key man risk. There’s 4 key men here, driving an organization of over 1000 employees with a diverse group of customers, but in the odd event that they would all leave or something bad would happen to them, it might affect the companies results going forward.

Conclusion

DBA is a solid Italian small growth company trading at a depressed valuation of 4x forward owners’ earnings. The prospects for the company look very positive, as it is well positioned to capture growth datacenters, energy transition, and cyber security. We are happy with the company’s capital allocation framework, with most of the profits being used to buy back stock at low valuations.

Disclosure: We still own DBA and this is not investment advice.

Disclaimer

This publication’s authors are not licensed investment professionals. Nothing produced by the Floebertus team should be construed as investment advice. Do your own research.

Nice. Short sweet writeup, looking forward to more of your content. Big fan of your work on Twitter 👏🏻🙌🏻